Student Loans: A Comprehensive Guide for Today’s Students

Understanding student loans is crucial for students today. A well-rounded knowledge of these loans can help shape your university journey. The student loan system plays a crucial part in higher education in the UK. It is designed to make further education accessible for everyone.

This blog aims to shed light on the critical aspects of student loans. We will unravel the complexities of the UK student loan system. It’s a comprehensive guide written in simple language to help you understand better.

Different Types of Student Loans

Maintenance Loans

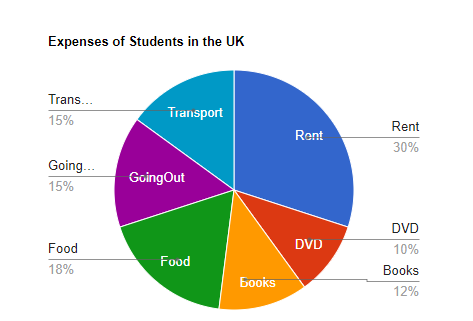

The other primary type of student loan in the UK is the Maintenance Loan. It helps with your living costs while you’re studying—things like rent and food.

Eligibility depends on factors such as your course, university, household income, and whether you’re living at home. The amount you can borrow varies. For the 2023/24 academic year, if you’re living at home, you could get up to £8,171.

Repayment for a Maintenance Loan follows the same rules as a Tuition Fee Loan. The interest rate is linked to inflation (RPI) plus up to 3%, based on income.

Expected Maintenance Loan Amounts (based on household income)

| Household Income (£) | Expected Maintenance Loan Amount for Students Living Away from Home (Outside London) (£) |

| 25,000 or less | 8,700 |

| 30,000 | 8,009 |

| 35,000 | 7,319 |

| 40,000 | 6,628 |

| 45,000 | 5,938 |

| 50,000 | 5,247 |

| 55,000 | 4,557 |

| 60,000 or more | 3,867 |

Tuition Fee Loans

It’s designed to cover your university or college fees. Students under 60, studying for a first degree or specific postgraduate courses, are eligible. Applying for this loan is straightforward. You can do it online via the official student finance website.

You start repaying once you earn over the income threshold. It’s currently set at £27,295 a year for plan 2 borrowers. Payments are 9% of your income over this threshold. Your employer usually manages this process through the tax system. Rest assured, any outstanding debt gets written off after 30 years.

There are exceptional cases too. Contrary to popular belief, a bad credit score doesn’t shut all the financial doors. Some lenders offer various types of credit facilities, including a pound 3000 loan for bad credit. Such options can help students maintain their education, despite their financial history.

Other Loans

| Type of Loan | Repayment Term |

| Postgraduate Master’s Loan | Begins once the graduate earns more than £21,000 per year, repayments are 6% of income over this amount |

| Postgraduate Doctoral Loan | Begins once the graduate earns more than £21,000 per year, repayments are 6% of income over this amount |

Applying for Student Loans

Applying for student loans in the UK is a process made user-friendly. It’s all done online through the Student Finance website. Start by creating an account. It’s straightforward. Be sure to keep this information secure.

You must provide details about your course, university, and personal circumstances. This is so they can determine how much loan you’re eligible for. It’s essential to have certain documents handy.

However, what if you encounter additional financial needs outside your regular student loans? What if, for instance, you’re grappling with a bad credit score and require a 1000-pound loan for bad credit?

Several lenders specialise in assisting individuals with poor credit histories. They offer various solutions, such as 1000 pound loans for bad credit. While the interest rates may be slightly higher, these loans can serve as lifelines for students needing immediate financial aid.

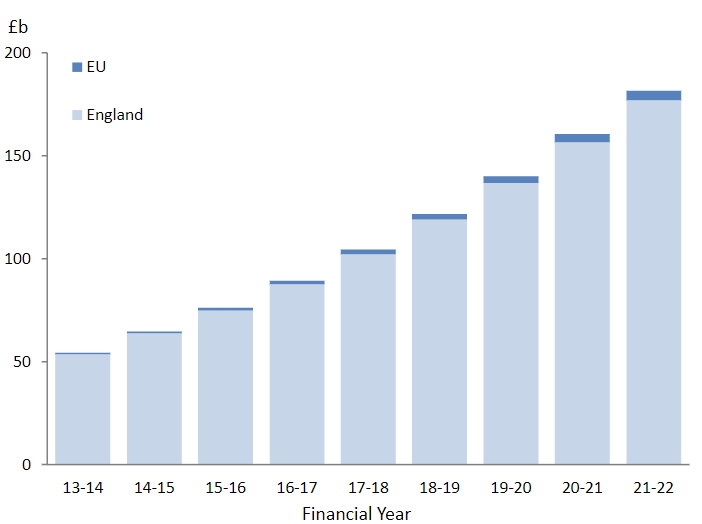

Student Loans in England: Financial Year 2021-22

Source: https://www.gov.uk/

Understanding Loan Repayment

Repayment Threshold and Income-Based Repayments

Getting to grips with UK student loan repayments is critical. A set income level, the ‘repayment threshold,’ triggers loan repayments. Currently, it’s £27,295 a year for those on plan 2.

Your repayments are worked out based on your earnings. Here’s how it goes. Earn over the threshold, and you’ll pay back 9% of anything above that level. Say you’re earning £30,000 annually. The amount over the threshold is £2,705. So, you’d repay 9% of this each year. That’s about £243.45 a year, or close to £20 per month.

What is the key point? Repayments link to income, not the loan size. It’s a system that adjusts to your income, keeping repayments in check with your financial situation.

Student Loan Interest Rates

| Loan Status | Interest Rate |

| While studying | RPI + up to 3% |

| From April, after leaving the course | RPI if income is £27,295 or less, up to RPI + 3% if income is £49,130 or more |

| Having left course | RPI + up to 3% until the loan is repaid in full |

Repayment Period and Loan Forgiveness

Let’s discuss the UK student loan repayment schedule and the idea of debt forgiveness. How long till the debt is paid off? It doesn’t last a lifetime. In the UK, student debts are forgiven after a set amount of time.

Does debt forgiveness exist? This occurs when the debt is discharged before the payback time is over. Additionally, when a borrower dies, the loan is often cancelled.

As a result, even though taking out student loans may seem like a significant commitment, the system is protected. The intention is to prevent the financial strain from becoming intolerable.

Exploring Part-Time Work and Other Income Sources

Perhaps a weekend job or a flexible role that fits around your lecture timetable would work best. Part-time work can help cover living expenses and reduce the amount you need to borrow. It also provides valuable work experience, a big plus when you graduate.

Part-time income may push you above the repayment threshold. But remember, it’s always based on what you earn over the threshold. It’s not a fixed amount and adjusts according to your income.

Exploring part-time work as a student is not just about earning money. It’s about gaining skills, experiences, and financial understanding. It’s about preparing for life after university.

Our Recommendation

Our top pick, Huge Loan Lender, excels as the UK’s best loan provider. Not only do they provide general loans, but they also specialise in student loans. This focus helps students in the UK navigate financial barriers effortlessly. Their system ensures simplicity and understanding. This gives them an edge over others.

By providing original, unique solutions, they stand out. Ultimately, this positions them as a trustworthy lender, especially when funding your education.

Conclusion

Understanding and managing student loans is a vital part of your university journey. Take proactive steps to get a grip on your finances. Then, craft a budget and savings plan. Explore part-time work if possible. These steps can significantly ease your financial journey.

For further information, the Student Loans Company and the Student Room offer a wealth of resources. Remember, student loans are not a burden but a tool. They enable you to pursue your academic dreams. With understanding and management, you can handle them confidently. So, go ahead. Dive into your academic journey armed with knowledge and assurance, knowing that your student finances are under control.

Ailsa Adam is the Editor-in-Chief and former content head at Hugeloanlender. She has been a valuable member of the content strategy team since 2017 due to her abundant experience in the finance sector. Passionate about helping individuals navigate the world of loans and personal finance, she has dedicated herself to acquiring extensive knowledge on various financial products. Before her role at Hugeloanlender,

Ailsa worked as a seasoned journalist and writer, specialising in creating informative blogs and articles on diverse loan types. She is known for her meticulous research and commitment to delivering accurate and engaging content. She holds a degree in MBA Finance and has a keen interest in creative writing and art.